Sign In

Get a Demo

Does the Accounting Standards Codification 842 (ASC 842) appear to be a little complicated to comply with?

While many organizational teams might find it a confusing element of the accounting regulations, a closer examination indicates that it is simple to understand. However, putting it into action could prove to be more challenging.

This guide, which covers the main components of ASC 842, is an effort to dissect this lease accounting aspect and analyze the modifications and long-term impact it could have on a company’s balance sheet. So, let's dig deeper.

Under the new ASC 842, businesses are mandated to register right-of-use (ROU) assets and liabilities for every lease, whereas, under the prior standard, most leases didn't get reflected on the company's balance sheet.

The Financial Accounting Standards Board (FASB) came out with the lease accounting standard ASC 842 with the intent to take the role of the previous lease accounting standard ASC 840.

The ultimate goal of Accounting Standards Codification 842 is to promote transparency and accountability in the leasing responsibilities of companies of all types, including public and private ones.

Investors, suppliers, government entities, and other business stakeholders now find it much more convenient, as a result of these modifications to financial statements, to carry out two things:

Furthermore, ASC 842 is quite comparable to the new international accounting standard for leases, known as IFRS 16, with regard to the definition of a lease.

This results in more comparable financial reporting for firms with lease assets in the United States and internationally.

Hence, the aggregate declared liabilities and assets on a corporation's balance sheet will now include all of the leases that have been recorded in accordance with ASC 842. It will result in major changes to the financial statements of the organization.

ASC 842 describes leases as contractual agreements, or segments of contracts, that award control or the right of use (ROU) of a physically distinguishable asset for a particular amount of time in return for compensation.

Leases can be for the entire asset or just a fraction of the asset.

Within the context of this definition, the term "control" conveys a specific connotation.

A corporate entity needs to be in a situation to gain a comprehensive economic benefit that results from the utilization of the asset and direct how it gets employed during the contract duration to establish control over an asset.

The asset that has been identified may be real estate, plant, machinery, or even other types of tangible assets. Instead of time, the duration of the lease period might also be expressed in relation to the degree of usage for the specified asset.

For instance, the period can be represented as the number of production units a machinery could be utilized to manufacture.

Although ASC 842 covers a substantial proportion of leases and subleases, there are some exceptions.

Generally speaking, ASC 842 should be applied to all leases and subleases, although there are several exceptions. Some instances when a lease gets included in a contract, yet ASC 842 (Subtopic 842-10-15-1) does not apply are as follows:

The new lease accounting standard comes into effect at separate junctures for publicly and privately held businesses.

The FASB standard became applicable to publicly owned companies for accounting periods that started after December 15, 2018. This implies that the standard was implemented on January 1, 2019, for calendar year-end organizations.

Private firms and non-profit corporations with annual reporting periods commencing after December 15, 2021, must comply with ASC 842.

This implies that many private and non-profit groups have already transitioned to this lease accounting standard in preparation for the year-end of 2022.

Before the implementation of ASC 842, operating leases were buried in the details of financial statements.

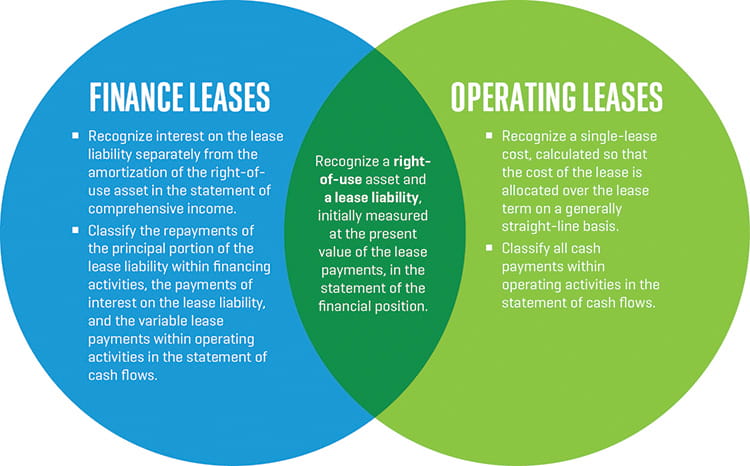

At this time, every operating lease must be accounted for on the company's balance sheet. The expense of the lease is often recorded as a single amount and distributed evenly along a straight line during the lease term.

The first thing to be accomplished is to calculate the lease liability and right-of-use (ROU) asset balances for precise accounting of operating leases in accordance with ASC 842.

To comply with the requirements of this dual-model technique, finance teams are required to track both the lease liability and the right-of-use asset, in which:

The lease liability is a financial liability that outlines the lease payments, interest costs, PV lease payment, and ending balance.

The image below depicts the formula for measuring ROU assets:

A company's finance team would want to evaluate the ROU asset using an amortization method that relies on the difference between the periodic straight-line lease cost and the interest. This will allow them to measure the ROU asset accurately.

The straight-line expense inclusion on the income statement is intended to illustrate how a lease directly affects a company's ability to generate cash flow throughout a specific period.

Let's understand operating lease accounting compliance with ASC 842 using an example.

A startup company is looking to lease a lot of computers for its office employees. The team contacts a business that rents out computer equipment.

Then, the leasing company's staff provides an operating lease pricing for twenty computers, with the company's staff taking care of all necessary upkeep, security, backups, and technical problems on behalf of the startup's team.

The company quotes lease payments at $1,500 per month, with the start of the four-year term set for January 1, 2022. However, there is an additional one-time setup fee of $1,000 charged by the leasing business to set up the machines.

In light of this constraint, they are offering the firm a software package with a licensing cost of $2,000, a significant discount for a company of their size.

The startup's finance department uses this information to swiftly calculate the following:

They determine their first month's leasing liability and ROU asset. What they find is as follows:

The team evaluates what these values are at the conclusion of one month to determine how much they will change over time.

The team then adds the interest to their principal lease liability balance, which can be added to the lease liability and subtracted from the ROU asset along with their routine payments. After that, they find:

Lessees are required to do the following when accounting for finance leases:

In accordance with the guidance, pre-existing capital leases are not required to undergo revision or reassessment upon transition, assuming that they get reported for appropriately following ASC 840.

As a result, the method of accounting of a capital/finance lease commencing before the transition will be comparable to the accounting treatment that is needed after the transition, and there is no need for any transition accounting modifications to be made.

One of the few exceptions to this rule is if there are any deferred or prepaid rents involved with the capital/finance lease when the transition takes place.

Any unpaid balances of deferred or prepaid rentals would be accounted for as revisions to the ROU asset that is associated with them.

According to ASC 842, at least one of the following requirements must be met for a lease agreement to be considered a financial lease:

Now, let's take a look at an example of finding whether a particular lease is classified as a finance lease following ASC 842.

Let's say that a corporation (the lessee) decides to rent a forklift with the accompanying stipulations attached to the lease:

Considering this example and the criteria discussed above, criteria 1 to 4 don't get satisfied.

Now, calculating the present value of the lease payments aggregate, the present value comes out to be $15,292.65. This figure is unquestionably higher than 90% of the asset's fair value ($14,400).

Hence, this lessee has selected the 90% criterion to indicate "substantially all" of the asset's fair value. This lease thus meets the fifth requirement for a finance lease and necessitates the use of finance lease accounting.

Leveraging a software solution to handle the transition to ASC 842 is a great investment for businesses as they adapt to the new GAAP lease accounting landscape.

The best ASC 842 lease accounting software will fulfill the business requirements in several key areas, including efficiency, convenience, customization, and security. Thus, businesses must invest in employing the leading tech solutions while accounting for leases.

LO is a cloud-based lease management softwarehere you can track, manage, and centralize all your lease data in ONE place. With LeasO, you can take care of all the compliances and complex ASC 842 lease accounting calculations right inside it to avoid any manual accounting error. Book a demo to know more.

.jpg)

Please submit your details and our Product Consultant will connect with you to understand your needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}